Wise investors know not to blindly put all their eggs in one basket. Instead, they become familiar with a few different types of investments and use their knowledge of each to make money in different ways.

When it comes to investing, there are a lot of baskets to choose from.BUT, it’s important to understand all your options before you actually invest your money and start to build your portfolio.

Every type of investment has its upside and downside. The best types of investments to make depend on your risk tolerance, level of understanding of certain markets, timeline to avoid capital gains, and reasons for investing in the first place.

Among the different types of investments out there, there are probably a few that will work well for you so let’s get into it.

Cash and commodities are typically considered low-risk types of investments, so if you’re new to investing or are very uncomfortably with any risk, one of these options could be a good place to start. Keep in mind that low-risk investments also tend to have low returns.

1. Gold

Yes, you can invest in gold and other commodities such as silver or crude oil. In fact, the practice of investing in gold goes way back, but that doesn’t necessarily mean it’s a great investment. Gold is a commodity, so its price is based on scarcity and fear, which can be impacted by political actions or environmental changes.

If you are investing in gold, be aware that your “moat” (protection against a price drop), is based on external factors – so the price can fluctuate a lot, and quickly. The price tends to go up when scarcity and fear are abundant and down when gold is widely available.

If you think the world is going to be a more fearful place in the future, then gold could be a good investment for you.

Key Takeaway: The thing to remember is that betting on commodities such as gold is usually just that — betting. It’s not Rule #1 Investing unless you KNOW that scarcity is going to create a demand for gold and drive up the price.

2. Bank Products and CDs

Bank products are investment types offered by banks that include savings accounts and money market accounts. Money market accounts are similar to savings accounts, but typically earn higher interest rates in return for higher balance requirements.

A CD, or certificate of deposit, is another type of bank product. When you purchase a CD you agree to loan the bank an amount of money for a designated amount of time in order to earn a higher amount of interest on it than you would in a typical savings account.

CDs are an extremely low-risk investment – but with low risk, comes low reward. Most banks offer CDs at a return of less than 2% per year, which is not even enough to keep up with inflation.

Key Takeaway: Don’t waste your time on CDs. While they can be a safe place to save your money and get a little more interest than you would in a savings account, they aren’t a great place to grow your money.

3. Cryptocurrency

Cryptocurrencies are one of the newer types of investment. They are unregulated digital currencies bought and sold on cryptocurrency websites.

Cryptocurrencies, such as Bitcoin or Dogecoin, have gained a lot of interest in recent years as an investment vehicle due to their quick and dramatic growth. However, they remain an incredibly risky investment because of the many unknown factors associated with them.

There is the possibility of government regulation and the possibility that cryptocurrency will never see widespread acceptance as a form of payment. Cryptocurrency currently has no intrinsic value and it could disappear as quickly as it came into existence.

How to Invest in Bitcoin

In the same way that you are able to exchange US Dollars for any other currency such as Yens or Euros, you can also exchange your US Dollars for cryptocurrencies.

Though cryptocurrencies aren’t technically part of the Forex market, the mechanics of investing in cryptocurrencies is very similar. The hope of many cryptocurrency investors is that the value of those cryptocurrencies goes up against the dollar, and they are relatively simple to buy online.

Someone who invested in Bitcoin in 2013 and sold it today would certainly make some incredible profits. The problem is that there’s no way to time the cryptocurrency market. Bitcoin and other cryptocurrencies could continue to dramatically increase in price, or they could drop to zero.

Key Takeaway: Take my advice and stay away. At this point, no one knows for sure what the future holds for cryptocurrencies, so investing in cryptocurrencies is little more than speculation. We don’t invest in things we don’t understand because that’s just gambling.

Bonds and Securities

Bonds and securities are other types of low-risk investments. Bonds can be purchased from the US government, state and city governments, or from individual companies.

Mortgage-backed securities are a type of bond that is typically issued by an agency of the U.S. government, but can also be issued by a private firm.

4. U.S. Savings Bonds & Corporate Bonds

When you purchase any kind of bond, you are loaning money to the entity you purchase it from for a predetermined amount of time and interest.

Bonds are considered safe and low risk because the only chance of not getting your money back is if the issuer defaults. U.S. saving bonds are bonds backed by the U.S. government, which makes them almost risk-free.

Governments issue bonds to raise money for projects and operations, and the same is true for corporations who issue bonds.

Corporate bonds are slightly more risky than government bonds because there’s more risk of a corporation defaulting on the loan. Unlike when you invest in a corporation by purchasing its stock, purchasing a corporate bond does not give you any ownership in that company.

An important note to remember is that a bond may only net you a 3% return on your money over multiple years. This means that when you take your money out of the bond, you’ll actually have less buying power than when you put it in because the rate of growth didn’t even keep up with the rate of inflation.

Key Takeaway: There is nothing “safe” about running out of money in retirement because your rates of return couldn’t keep up with inflation while you were trying to grow and protect your money. It’s not worth it to put your money in bonds.

5. Mortgage-Backed Securities

When you purchase a mortgage-backed security, you are once-again lending money to a bank or government institution, but your loan is backed by a pool of home and other real estate mortgages.

Unlike other bonds, which pay the principal at the end of the bond term, mortgage-backed securities pay out interest and principal to investors monthly.

Key Takeaway: While they can be a type of income investment that provides steady returns, mortgage-backed securities are one of the more complex investment types, and so should be avoided by beginner investors.

Investment Funds

Investment funds are made up of a pool of money collected from multiple investors that are then invested into many different things including, stocks, bonds, and other assets. The collection of investments typically tracks a market index.

6. Mutual Funds

A mutual fund is a type of investment fund operated by a money manager who invests your money for you, and attempts to get good returns.

Mutual funds are typically made up of a combination of stocks and bonds, however, they carry less risk because your money is diversified across many stocks and bonds. You’ll only reap rewards from stock dividends and bond interest, or if you sell when the value of the fund goes up with the market.

The average individual will need more than $3 million to be financially independent in retirement in twenty years and, frankly, mutual funds won’t get you there.

When it comes to value, remember that mutual funds are built and managed by so-called “financial experts” who have a hard time beating the market, especially when you factor in the fees they’re charging you to manage your money in the first place.

Rule #1 Investors expect a minimum annual compounded rate of return of 15% a year or more. If we can get that, we don’t care what the market did because we’re going to retire rich anyway.

Key Takeaway: You’ll have a much easier time (and more fun!) learning how to invest your own money rather than relying on some mutual fund manager who can’t beat the market.

7. Index Funds

Similar to mutual funds, index funds are one of the types of stock investments that diversifies your investment across multiple stocks. The difference between index funds and mutual funds is that index funds are passively managed, not directly overseen by a money manager.

Because index funds are passively managed, there are less fees involved, which means you have the potential for slightly higher returns than with a mutual fund. However, your returns will be based entirely on how well the index your fund is tracking does.

Given that most major indexes are used to track the overall movement of the market, they perform about as well as the overall market does in the very long term. In other words, they tend to yield an average return of about 7% per year.

While this isn’t as high as the returns you can achieve through successfully picking individual companies with the right research, it IS a respectable return that is considerably higher than the interest rates of a savings account or the return rates of bonds.

When you invest in an index, you’re essentially betting your money on the future of America. If you’re confident the American economy will keep growing, you’re probably going to come out ok.

The problem here is that if you put your money into an index, and we go into a recession, the market could be down for a significant amount of time. That means your portfolio will also be down, and if you’re too close to retirement to wait for things to swing back the other way, you could be in trouble.

That’s another plus of investing in individual companies. The really great ones tend to perform, even in times of recession.

Key Takeaway: If you don’t want to do the work (and reap the rewards) of learning to invest in individual companies, an index fund is a good “put your money in and forget about it” option that will typically generate better results than a mutual fund.

8. Exchange-Traded Funds

Exchange-Traded Funds, or ETFs as they’re commonly called, are similar to index funds in that they track a popular index and mirror its performance. Unlike index funds, though, ETFs are bought and sold on the stock market.

Because ETFs are traded on the stock market, you have more control over what price you purchase them at and will pay fewer fees. Your reward is completely dependent on how well or how poorly the index you invest in performs.

You can minimize your risk by investing in an ETF that tracks a broad index, such as the S&P 500.

Simply putting your money in an exchange-traded fund like the S&P 500 (SPY), a collection of the 500 biggest companies in the market, allows you to profit from the market’s growth without having to pay fees to a fund manager.

Key Takeaway: Aside from investing in individual companies, an ETF is probably the best option beginner investors have available.

The Stock Market

There are a number of ways to invest in the stock market. As I mentioned above, you could invest in a stock market index, or you could invest with stock options, or—and this one’s my favorite—you could invest in individual stocks.

9. Individual Stocks

Stocks are “shares” of ownership in a particular company. When you purchase an individual company’s stock, you become a partial owner of that company. That means when the company makes money, so do you, and when the company grows in value, the value of your stock grows as well.

When the price of a company’s stock goes up, the value of the owner’s investment in that company goes up. The owner can then choose to sell the stock for a profit. However, when the price of a company’s stock goes down, the value of the owner’s investment goes down.

Stock owners can also receive rewards via dividends if the company chooses to distribute earnings to their shareholders.

It is possible to achieve much higher than average returns by investing in hand-selected individual companies you’ve researched. You can minimize your risk by investing in only wonderful companies at prices that guarantee a big return. That is the Rule #1 way.

Key Takeaway: Among the many things to invest in, stocks are my personal favorite and by far the most rewarding. The most successful investors invest in stocks because you can make better returns than with any other investment type. Warren Buffett became a successful investor by buying shares of stocks, and you can too.

10. Stock Options

When you purchase an option in a company, you are betting that the price of that company’s stock will go up or down. Purchasing an option allows you to buy or sell shares of that company at a set price within a set timeframe, without actually owning the stock.

Stock options are incredibly risky. As with most high-risk types of investments, there is potential for high returns. Unfortunately , there is also the potential for great loss – especially if you don’t know what you’re doing

Put Options

With a PUT option, you’re agreeing to SELL a stock when it gets to a certain price at a specific time. With a CALL option, you’re agreeing to BUY a stock at a certain price at a specific time.

PUT options can be thought of like insurance policies. You get them at a set price, over a certain period of time and sell the stock regardless of the price. Investors generally buy PUTS when they are concerned that the market will fall. This is because a PUT gives you the right to sell a stock at a fixed price, and it will typically increase in value if the price of the underlying stock starts to drop.

Call Options

CALL options have a market price, referred to as a premium. You pay the premium of the call option to secure the contract to buy the underlying stock.

Investing in CALL options is a fantastic way to generate cash flow and reduce basis on companies we already own.

Key Takeaway: In addition to stocks, options are a good choice if you are looking for high-return types of investments. However, I don’t recommend investing in options for beginners.

Retirement Plans

There are two major types of retirement accounts: a 401K and an IRA. Both accounts are made up of cash you put aside and then invest in various ways.

The risk and reward of retirement accounts are completely dependent on what they are invested in, which can vary greatly. In addition to these retirement accounts, annuities are another investment type that you may want to consider as part of your retirement plan.

11. 401k

A 401k is a retirement account offered by your employer. The big benefit of this retirement option is that your employer may offer a “match”, which means they will match the amount of money you put into your account – up to a certain percentage.

The Big Problem with 401ks

All of the money invested in a 401(k) ends up in mutual funds. The problem is that these mutual funds almost always fail to outperform the market average.

In other words, simply putting your money into an index such as the S&P 500 and leaving it there with zero management would still net you more returns than you are likely to see when you invest in a 401(k).

The reason why mutual funds fail to outperform the market once again goes back to the fact that the managers of these funds charge a considerable fee for their services. Once this fee is deducted, any returns that the manager was able to yield beyond the overall market’s performance are quickly diminished.

Remember, diversifying your investment portfolio does not inherently mean that you are lowering your potential for risk.

Key Takeaway:

401ks are not something that should be avoided in all situations. An employer match that doubles your investment is almost always worth it. However, they should not be relied on as your sole means of investment.

Stick to the employer match. Investing any more than that in a 401k is just a wasted opportunity.

12. IRA

An IRA is an individual retirement account you can set up for yourself. In terms of IRAs, there are traditional IRAs (tax-deferred) and Roth IRAs (is tax-free).

Yes, you read that correctly. A Roth IRA is tax-free!

The money you invest in a Roth IRA is taxed before it is invested, so when you take it out during retirement you aren’t taxed on the income from your investments.

With both an IRA and a Roth IRA, you have more control over where you invest your money than you do with a 401K. You can choose to invest the money in these accounts in individual stocks, bonds, ETFs, and mutual funds.

The more control you have over your investments and the more diversified they are, the less risk you face.

Key Takeaway: No matter who you are or where you work, a Roth IRA is one of the best things to invest in because you can have total control over what it is invested in and your money grows tax-free! Max it out and invest it the Rule #1 way.

13. Annuities

Annuities are a contract between an investor and an insurance company where the investor pays a lump sum in exchange for periodic payments made by the insurer. They are typically used to supplement income and lock down a steady monthly payment during retirement.

There’s no real risk to annuities, but there’s no real chance of return either. They are simply a way to set aside income for retirement, not ensure growth.

Key Takeaway: While annuities may be helpful for some retirees, they are not an ideal investment option for beginner investors who are looking to actually grow their money.

Real Estate

There are a variety of ways to invest in real estate from buying homes, apartments, and commercial business buildings to flipping houses, or even owning farms and trailer parks.The main drawback for most beginning investors is that the price of entry is high.

14. Property

Property is often an expensive investment, which can easily crowd out small investors with less capital.

However, crowd-funded real estate investment opportunities are beginning to pop up, providing new types of investments for those who want to invest in real estate but don’t have all the cash.

The hardest part about investing in real estate is finding a property that you can purchase with a margin of safety. If you can do that, you can make some decent returns investing in property.

You can make money by buying the property at a below-market rate and selling it at full price, as well as by renting or leasing the property to tenants.

The various types of property investments can all be good, as long as you treat them the same as any other Rule #1 investment. This means the property should have meaning to you, have a moat, good management, and be purchased with a margin of safety.

Key Takeaway: While it’s possible to find a great deal on real estate, it might be easier to invest in the stock market, make the same returns or better, and not have to deal with having a bunch of rental properties to take care of.

15. Real Estate Investment Trust

A Real Estate Investment Trust, or REIT, is similar to a mutual fund in that it takes the funds of many investors and invests them in a collection of income-generating real estate properties.

Plus, REITs can be bought and sold like stocks on the stock market so they can be cheaper and easier to invest in than property.

Without having to buy, manage, or finance any properties yourself, investing in a REIT reduces the barriers of entry common to property real estate investment.

Key Takeaway: You don’t need a lot of money and you don’t need to worry about maintaining the properties. While you won’t make as much money from property appreciation, you can receive a steady income from REITs.

What Are the Worst Types of Investments for Beginners?

While it makes sense to ask what you should invest in, it may be even more important to know what not to invest in.

A good rule of thumb as a beginner is: If you’re putting a lot of money into it but not getting anything out of it other than a bunch of debt or an ego boost, it’s a bad investment.

This includes expensive cars, fancy interiors, and other items that decrease in value over the period of time you own them.

While fancy material things may help you keep up with the Jones’ on your block, the benefit is ultra temporary. It’s so important to live within your means and spend your money wisely so you can afford the life you want in the future.

Avoid these common money traps and you’ll have more money for the good things to invest in both now and in the future.

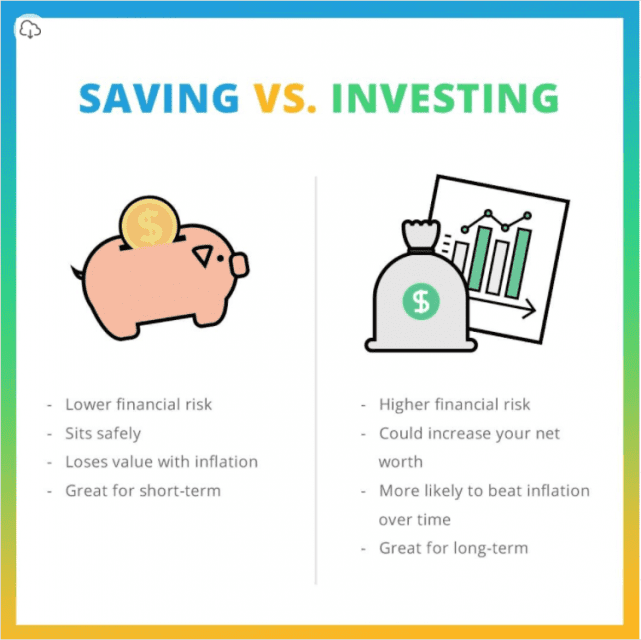

Warning: Putting your money into expensive possessions or setting it in a savings account because you think it’s “safe” will only hurt you in the long run.

None of these are investments—they’re money traps. Like cars and boats, money sitting in a savings account is losing value over time. Put your money into the only type of investment that’s guaranteed to make you money—the stock market.

What Are the Best Types of Investments for Beginners?

Everyone’s reasons and personal risk tolerances are different, so you have to decide for you which investment types suit your lifestyle, timeline, and goals best.

I’m not your financial advisor, and this is for entertainment purposes ONLY — but here’s what I would do:

First, I’d open up a Roth IRA and invest for retirement so my money can grow tax-free.

Then, if I just wanted to invest my money with little research and forget about it, I’d put a chunk of it into an Index Fund such as the S&P 500 or the Russell 2000.

Lastly, but certainly not the least of these, I’d invest in the stock market.

We’ll get into how to invest in stocks in later chapters. But it’s important to note that of all types of investments we covered – the stock market is the best place to invest with a small amount of money and still get big returns.

Phil Town is an investment advisor, hedge fund manager, 3x NY Times Best-Selling Author, ex-Grand Canyon river guide, and former Lieutenant in the US Army Special Forces. He and his wife, Melissa, share a passion for horses, polo, and eventing. Phil’s goal is to help you learn how to invest and achieve financial independence.

I’m a full-time investor and 3x New York Times best-selling author. I want to help the little guys, people like you and me, gain financial freedom by using simple principles that Warren Buffett and Charlie Munger have been using for over 80 years.

I have a passion for investing and I can’t wait to share it with you.